If you recently took out a mortgage, or have been thinking about purchasing real estate, you may be wondering when your mortgage payments will be due each month, among other things (like how late Ikea is open).

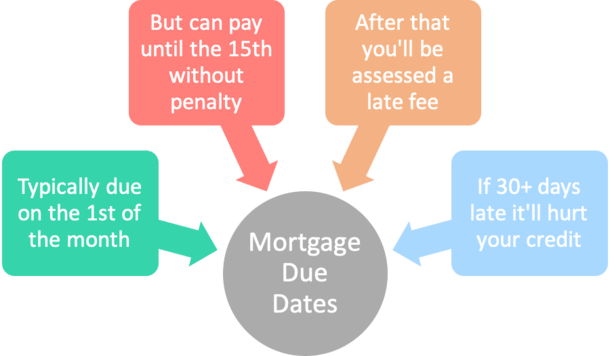

Well, mortgage payments are generally due on the first of the month, every month, until the loan reaches maturity, or until you sell the property.

So it doesn’t actually matter when your mortgage funds – if you close on the 5th of the month or the 15th, the pesky mortgage is still due on the first.

The only difference is when the first mortgage payment is due, which I’ve explained in my when mortgage payments start post.

Most people probably know that mortgage payments are due on the 1st of the month, but many loan servicers (those who collect your payments) will allow you to pay 15 days “late” each month.

So even though your mortgage payments are technically due on the first each month, you can pay as late as the 15th every month without any kind of penalty.

No late fees, no credit report dings, no issues whatsoever.

This is known as the “mortgage grace period,” similar to other grace periods you see with all types of other loans.

Some “savvy” consumers may even set up automatic payments to be sent mid-month, instead of paying on the first to maximize their cash flow.

But this can be a dangerous game, especially if your mortgage payment doesn’t make it to the servicer on time, for whatever reason.

Nowadays, this may be less of a problem thanks to speedy and generally reliable online payments, but it’s still a risk not worth taking.

The loan servicer may also harass you if you consistently pay late into the grace period.

As seen in the Closing Disclosure (CD) screenshot above, payments are typically only considered late if they’re more than 15 days late.

Check your own paperwork (on page 4 of the CD) to see if the same terms apply to your home loan.

Just note that if you play this “pay at the last minute game” each month, you could eventually get burned and wind up paying a mortgage late fee.

These fees can vary, but are often pretty steep. We’re not talking a $20 late fee and a slap on the wrist.

We’re talking a percentage of the mortgage payment, such as 5%. So if your monthly mortgage payment is $3,000 a month, that’s $150 smackers.

And if you wait too long to make a payment, typically 30+ days beyond the due date, it could eventually be reported to the credit bureaus as a late payment, which will really hurt.

The result could be a substantial credit score ding, and greater difficulty obtaining subsequent mortgages in the future, a major issue if you need/want to refinance your home loan for some reason.

Or if you want to buy more real estate in the near future.

After all, lenders aren’t too fond of homeowners who don’t make their mortgage payments on time.

Okay, so we know paying late isn’t too smart, but what about paying the mortgage before the due date?

You might be thinking, “Hey, I can save money on interest if I make my payments on the 20th or 25th of each month, instead of the first of the next month.”

Not the case. Your loan servicer may accept payment on that date, but it won’t mean you’ll pay less interest.

The interest is already figured out for the month using the previous month’s balance, so it doesn’t matter if you pay a few days early.

This differs from credit cards and other types of loans, such as HELOCs, where the interest is calculated daily.

If you actually want to pay less in interest on a traditional mortgage, you need to make extra payments to principal.

So if you pay an additional $100 on top of your monthly mortgage payment, your loan balance will be $100 lower for the subsequent month, and that means less interest paid over the life of the loan.

This will also reduce the loan term, meaning your mortgage will be paid off in less time.

Just note that the monthly mortgage payment will stay the same, regardless of whether you make larger payments for a few months here and there.

Tip: Be careful when making extra principal payments. If you send in a payment that is below the monthly mortgage payment, such as two smaller biweekly payments, even if they exceed the total amount due, they may not be credited properly.

Lastly, let’s talk about how to make a mortgage payment to your loan servicer.

First things first, note that I said loan servicer, not lender or broker or any other entity.

The “loan servicer” is the company that actually collects your mortgage payment each month, and may not be the individual or company that originated your loan.

So pay close attention to who this is, and note that mortgage loans are often transferred from one servicer to another, especially shortly after closing.

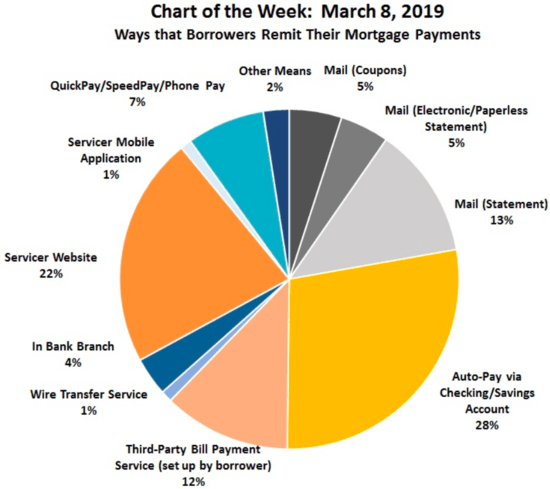

In terms of paying, we see from the graphic above (from the Mortgage Bankers Association) that lists the most common ways to pay a mortgage.

The top three are auto-pay, via the servicer website, and by mail.

Less common ways are in-branch, wire transfer, phone pay, and other means, which probably includes paying the mortgage with a credit card.

In summary, speak with your loan servicer once you take out your mortgage to ensure your payments are processed properly. Rules vary and it’s best to get all the answers straight from the horse’s mouth.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.

Latest posts by Colin Robertson (see all)